Senegal Series Part 5: International Borrowing and the Persistence of Colonial Revenue Constraints - Ghana and Senegal in Comparative Perspective

This is the final part of a four-part series applying the Hausmann-Rodrik-Velasco growth diagnostics framework to Senegal. Part 0 introduced the diagnostic method. Part 1 showed that Senegal's structural transformation produced employment reallocation without productivity gains. Part 2 ruled out human capital as the binding constraint. Part 3 identified electricity and labour regulation as the primary constraints, but noted that Senegal's chronic fiscal fragility operates as a meta-constraint, narrowing the government's capacity to fix anything else.

This post is based on an essay I wrote for the African Political Economy course DV435 taught by Prof. Catherine Boone at the LSE, whose own work on African state formation and elite coalitions is central to the argument. This post fits in the series by asking the obvious follow-up question: why is that fiscal capacity so thin, and why has six decades of international borrowing failed to build it?

Introduction

Through comparative analysis of Ghana and Senegal across two periods (1960-1980, 1980s-1990s), I argue that international borrowing substituted for rather than enabled overcoming development hurdles created by colonial revenue constraints.

This is not an argument against external financing or debt relief. A capital-scarce post-colonial state with a 15-20 percent fiscal gap had little alternative but to borrow. It is an argument about what borrowing could and could not do. While borrowing could fill the revenue gap, it could not dissolve the political coalitions that made building a domestic revenue base so costly

Colonial rule bequeathed two interconnected hurdles: first, a volatile and procyclical revenue system dependent on commodity prices that hindered productive investment; second, domestic coalitions (farmers, chiefs, religious authorities) with a veto power to limit the state's ability to impose politically costly direct taxation. While both countries achieved partial progress on fiscal vulnerability through export diversification and Value-Added-Taxation, coalition veto remained a determining obstacle.

The argument proceeds in four parts. Part I shows how these hurdles originated in colonial gatekeeper state structures and why international borrowing offered a politically expedient alternative to confronting coalitions. Part II traces the substitution pattern across two distinct periods: post-independence developmentalism (1960-1980), where favorable conditions for fiscal consolidation proved insufficient when coalitions blocked reform; and the structural adjustment era (1980s-1990s), where IFI conditionalities achieved only coalition-permissive reforms (VAT) while leaving direct taxation untouched. Part III shows that despite divergence across colonial legacies, political stability, resources, and adjustment outcomes, both countries reproduced the same borrowing substitution pattern after 2000, as debt relief, oil revenues, and creditor diversification each failed to break coalition veto power over direct taxation.

Selected Cases

Ghana and Senegal make for a revealing comparison precisely because they differ on almost every variable that conventional explanations would emphasise. They exhibit a number of differences in potentially determinative variables: colonial administration (British indirect versus French direct rule), political trajectories (Ghana’s coups versus Senegal’s civilian continuity), resource endowments (Ghana’s oil versus Senegal’s scarcity), structural adjustment outcomes (Ghana’s revenue rising 4.6 percent to 16.2 percent GDP versus Senegal’s stagnation), and creditor relationships (IFI engagement versusCFA constraints). Despite these differences, both shared similar starting points, gatekeeper structures with ~60-65 percent trade taxes, ~8 percent direct taxes at independence, and similar endpoints: debt crises worse than pre-HIPC by 2017-2024 with direct taxation at 5-6 percent GDP. Exogenous economic conditions varied over time: favorable 1960s, crisis 1970s, SAP conditionality, post-2000 creditor diversification, yet outcomes converged in both cases.

The fact that two countries so different in colonial history, political trajectory, and resource endowment arrived at the same fiscal outcome (direct taxation stuck at 5-6 percent of GDP and debt worse than before relief) points toward a common mechanism rather than country-specific explanations. I argue that the mechanism is the coalition veto interacting with the persistent availability of external finance. By grounding the analysis in historically specific coalitions rather than cultural deficiencies, it avoids African exceptionalism and situates Ghana and Senegal within political-economy dynamics visible wherever states lack the political capacity to tax domestic elites directly.

The Colonial Trap: Gatekeeper States and the Roots of Fiscal Weakness

The Gatekeeper State Revenue Structure

Both Ghana and Senegal inherited what Cooper (2002) conceptualizes as the gatekeeper state, meaning a fiscal and political structure in which governments derived revenue primarily from controlling the interface between domestic and international economies rather than from taxing domestic economic activity directly (Cooper, 2002, pp. 135-138; Gardner, 2012, p. 5). Revenue extraction was therefore concentrated at borders through trade and commodity taxation, producing volatile revenues and weak fiscal ties between states and societies.

In 1960, Ghana’s government revenue of ~£83-97 million derived approximately 65 percent from trade taxes, with income tax contributing only 7.9 percent (Economist Intelligence Unit [EIU], 1965, p. 9). Senegal similarly relied on trade taxation for approximately 60 percent of government revenue, which totaled just 12-14 percent of GDP, with the country recording negative domestic savings (World Bank, 1989, Table 2, p. 3). As Gardner (2012, p. 4) notes, colonial revenue systems were so narrow that most colonies couldn’t earn enough to run themselves.

Limited State Capacity and Elite Coalitions

Newly independent African states inherited limited administrative capacity of colonial institutions (lacking census data, property registries, and income tracking systems necessary for direct taxation) and the lack of legitimacy of central authority (Gardner, 2012, p. 113). Political authority resembled colonial-era decentralized despotism (Mamdani, 1996), rooted in coercive and administrative power rather than consent-based fiscal legitimacy, creating perceptions of the state as distant and extractive that reduced governments’ bargaining power over taxation (Cooper, 2002, p.138; Riddell, 1992, p.60). States remained dependent on elite support rather than broad-based fiscal incorporation. As Boone (2012) argues, uneven state reach was often “by design” – governments strategically limited fiscal penetration to preserve elite coalitions, reducing incentives to build broad-based taxation.

Crucially, the specific administrative machinery that would have drawn informal economic activity into the tax net (taxpayer registries, property cadastres, income tracking systems) was precisely the infrastructure the coalition had no interest in funding. A state capable of registering and taxing the incomes of smallholders, traders, and rural producers would be a state capable of taxing elites too. The failure to build that capacity was therefore not simply an inherited colonial deficit but the coalition veto operating on administrative investment. Informality persisted not because the state lacked the resources to see the interior, but because seeing it was politically threatening.

Despite independence and democratic elections, these gatekeeper structures persisted, allowing governments to avoid direct tax relationships with citizens (Cooper 2002, p. 240).

The Dual Development Hurdles

These colonial legacies imposed two interconnected development hurdles that international borrowing was expected to help overcome. The first development hurdle is a volatile and procyclical revenue system. This fiscal vulnerability hindered productive investments and triggered recurring crises. When commodity prices fell, as during Ghana’s 1970s cocoa collapse or Senegal’s 1972-74 drought, revenue collapsed simultaneously with export earnings, triggering immediate fiscal crises. This volatility prevented long-term investment planning and created recurring patterns of crisis and borrowing. Overcoming this hurdle would require a diversified revenue base with the majority of government income derived from domestic taxation, and one that would grow automatically with the economy, rather than fluctuating with global commodity markets.

The second development hurdle is a structural political constraint caused by inherited legitimacy structures and entrenched elite coalitions limiting the state’s ability to impose politically costly fiscal reforms. Postcolonial African states inherited distinct legitimacy structures in which political authority rested on negotiated rule and elite mediation rather than bureaucratic domination, imposing limits even on authoritarian governments’ ability to tax powerful groups directly (Cooper, 2002; Boone, 2003; Mamdani, 1996). In Ghana, cocoa farmers, traditional chiefs, and the civil service possessed effective veto mechanisms, electoral, economic (reducing production or capital flight), and coercive (strikes or coups when threatened) (Cooper, 2002). Nkrumah “feared farmers would become politically active,” constraining his ability to expand income taxation (Cooper, 2002, p. 138). In Senegal, the Mouridi Islamic brotherhood-controlled groundnut production and delivered rural votes, French commercial interests threatened capital flight, and urban elites depended on government spending. In 1979, when Senghor’s government was imposing increasingly more authoritative measures, “peanut farmers organized to set peanut prices very low and the state gave in,” demonstrating coalition power to force government capitulation (Cooper, 2002, p. 254). These coalitions’ economic interests and political power benefited from indirect taxation while blocking direct taxation of their incomes, property, and profits.

Crucially, these hurdles reinforced one another: fiscal volatility created pressure for reform, while elite coalition vetoes determined whether governments borrowed externally or expanded direct taxation. Persistent access to borrowing enabled repeated substitution for politically costly fiscal reform. The outcome this essay traces is whether international borrowing helped build a durable domestic revenue base, specifically, raising direct taxation as a share of GDP, with the ability to service debt without crisis as the downstream consequence of whether that succeeded or failed.

The Fiscal Gap and Borrowing Solution

Colonial fiscal systems were designed to sustain minimal public spending of around 10 percent of GDP, sufficient only for basic administration and export-facilitating infrastructure, while post- independence governments faced popular demands and nationalist commitments to expand education, healthcare, and infrastructure, raising expenditure toward 25–30 percent of GDP, characteristic of developmental states (Gardner, 2012, pp. 227, 241). Contrary to “anti- developmental state” narratives, early post-colonial African governments often actively expanded public spending, often tripling colonial-era levels, often tripling colonial-era levels to finance education and health as part of nation-building projects (Mkandawire 2001, pp. 289-292; Cooper, 2002, p. 172). This created a structural fiscal gap of 15-20 percent/GDP. International borrowing offered a politically expedient solution, allowing governments to expand services without confronting the politically costly task of building direct-tax-capacity, a pattern that began immediately after independence and persisted across subsequent decades (Cooper, 2002; Gardner, 2012; Jerven, 2010).

Pattern Recurring over Two Periods Borrowing Instead of Taxing

Period 1: Post-Independence Developmentalism (1960-1980)

Even though external conditions in this period were unusually favorable, both governments nonetheless turned early to external financing to support their developmental agendas. The first post-independence decade offered favorable conditions for fiscal transformation. Commodity prices remained relatively stable, with Ghana’s cocoa exports earning steady foreign exchange and Senegal’s groundnut prices benefiting from French guaranteed purchase agreements (EIU,1965, p.2-3; World Bank, 1989, Table 2, p.3). Cheap concessional credit flowed from former colonial powers and IFIs, while global “Big Push” development optimism provided technical assistance for state-building (Cooper 2002, pp. 127-128).

Ghana’s industrialization strategy in the early post-independence period was financed primarily through external borrowing, with little direct-tax expansion. Revenue structure remained essentially unchanged from the colonial baseline. Trade taxes comprised 65 percent of revenue, and income tax merely 7.9 percent (EIU, 1965, p. 9). In Ghana, elite control over land and production constrained fiscal incorporation (Boone, 2003, Ch. 4). Boone explains that “established rural elites, chiefs, aristocratic families, religious authorities, had a stake in defending and enhancing power already achieved” (2003, p. 6-7). Similarly, Cooper (2002, p.138) shows that Nkrumah feared political mobilization among farmers. These elite coalitions made direct taxation politically untenable even for a leader with Nkrumah's revolutionary ambitions. Given Nkrumah’s extensive development plans of building the Volta Dam and civil service expansion, the government borrowed massively. The interaction of fiscal pressure (development spending needs), and coalition blocking produced a borrowing substitution effect. External debt exploded eightfold from £22.9 million in 1959, to £183.6 million in 1963 (EIU, 1965, p. 10).

These substitution patterns intensified during the 1970s crisis decade. Despite global shocks such as oil price increases (1973, 1979), collapsing commodity prices, and rising interest rates following the Volcker shock, revenue structures remained fundamentally unchanged. In Ghana, trade taxes still comprised 48.6 percent of revenue (with cocoa export duties at 40 percent), while income tax contributed merely 21.6 percent (EIU 1980, p. 15). Export concentration persisted at 54-58 percent cocoa throughout the decade (EIU, 1980, p. 17). When the fiscal crisis intensified, successive military governments, none possessing sufficient political authority to confront farmers, chiefs, or the civil service, chose substitution. Domestic borrowing from the Bank of Ghana produced hyperinflation of 116 percent (1977) and 73 percent (1978), collapsing revenue as a share of GDP to just 4.6 percent by 1983 (EIU 1984, p. 16). By decade’s end, Ghana had accumulated $976 million in external arrears and effectively defaulted (EIU 1984, p.18).

Senghor’s Senegal pursued “economics and humanism” (Cooper 2002, p. 130) through different ideological framing, but similar results as Ghana’s substitution. Revenue structure remained around 60 percent trade taxes, with negative domestic savings recorded annually (World Bank 1989, Table 2, p. 3), showing spending exceeded all domestic revenue from day one. As in Ghana, fiscal and administrative penetration in Senegal was strategically limited, where powerful intermediaries controlled production and political order (Boone, 2003, Ch. 4, pp. 157–160). In this case, the Mouride Brotherhood, controlling groundnut production and delivering rural votes, remained politically untaxable, while French firms dominated trade networks and could credibly threaten capital flight (Cooper, 2002, p. 190). Given the political sensitivity of taxing the Mouride Brotherhood and French commercial interests, the Senegalese state relied on external borrowing from France and IFIs to finance infrastructure investment (World Bank 1989; Koddenbrock 2024, p. 1799).

The 1970s provided a crucial natural experiment for Senegal. If resource scarcity were a significant hindrance to fiscal transformation, then a temporary resource windfall from phosphate price increases (1974–1978) should have enabled fiscal transformation. However, when phosphate exports surged, temporarily diversifying Senegal’s export base beyond groundnuts and generating substantial revenues (World Bank 1989, pp. 2–3), the Diouf government (succeeding Senghor in 1981) used the windfall to finance urban infrastructure, civil service expansion, and agricultural subsidies, all of which preserved coalition support, while not investing in tax administration or confronting the Mouride Brotherhood to expand direct taxation. Despite the windfall, external debt rose from $110 million (1971) to $1.5 billion (1979) (World Bank 1989, pp. 2–3), showing that additional resources did not reduce borrowing or enable tax reform.

What Both Cases Tell Us

Despite different ideological orientations, colonial legacies, and political outcomes, both countries exhibited the same substitution patterns while maintaining indirect taxation to avoid confronting coalitions. The 1960s’ stable conditions and the 1970s’ extreme pressures – crisis in Ghana, windfall in Senegal – produced different forms of substitution, but in both cases, coalitions retained veto power, direct taxation remained minimal, and a severe fiscal crisis required IFI intervention in the 1980s. Senegal’s phosphate windfall is compelling evidence that temporary resource abundance did not produce fiscal transformation when coalition vetoes remained binding.

These cases suggest that in the early post-colonial period (1960-1970) domestic blocking coalitions, not resource scarcity or external constraints, constituted the binding constraint on fiscal transformation.

Period 2: Structural Adjustment Era (1980- 2000)

The 1980s-1990s structural adjustment era presents a potential challenge to the substitution thesis. During this period, IMF and World Bank programs explicitly recognized the significant role of the endogenous factors constraining development (Riddell 1992, p. 55). SAPs incorporated conditionalities targeting political economy constraints, including civil service retrenchment, agricultural taxation reforms, trade liberalization, eliminating protective marketing boards, and tax administration modernization (Riddell, 1992; IMF, 1995). Ghana and Senegal experienced radically different outcomes to these programs. Ghana’s revenue rose from 4.6 percent to 16.2 percent of GDP (1983-1994), while in Senegal, revenue declined from 19.8 percent to 17.8 percent. Nevertheless, both exhibited identical deeper reform-blocking patterns from domestic coalitions.

Ghana’s revenue growth reflected Rawlings’ authoritarian capacity rather than coalition breaking. Revenue surged to 16.2 percent of GDP, with Rawlings’ military government imposing austerity (IMF, 1995). However, improvement happened via indirect-to-indirect substitution, meaning trade taxes fell from 52.6 percent to 28.5 percent of revenue, but Value-Added-Taxes rose, while direct taxes remained stagnant at 13.4 percent (IMF, 1995, Table 9, p. 60). This way, Rawling avoided coalition confrontation. Cocoa farmers retained marketing board protection, chiefs maintained land control, and the public sector preserved employment. When Rawlings faced elections (1992), he raised civil service wages “against IMF advice” (Cooper,2002, p. 244), suggesting that authoritarian capacity under adjustment was short-lived, and that the return to electoral competition quickly restored coalition veto power over fiscal policy.

Senegal’s “failure” under SAPs reflected civilian constraints rather than different dynamics. Revenue declined to 17.8 percent of GDP, with the only major tax reform being the VAT introduction in 1988 (Independent Evaluation Office [IEO] of the IMF, 2002, Appendix II, p. 192) – the same substitution as Ghana. While the SAPs weakened the economic bases of rural elite control, their political role as intermediaries between the state and the peasantry persisted. The result was an adaptation rather than a coalition rupture that could result in an increase in direct taxation (Boone, 2003, p. 337).

What Both Cases Tell Us

Although SAPs altered some crucial aspects of state administration, they failed to produce lasting changes in revenue structures because entrenched political economy constraints shaped how reforms were implemented. In addition to implementation constraints discussed by Riddell (1992, p. 63), the evidence points to two main reasons why international borrowing during SAPs didn’t remove development hurdles.

First, democratization strengthened the veto power of the elites. The 1990s “dual liberalization” produced contradictory effects. IFIs assumed democracy would create downward accountability, but it formalized coalition electoral veto instead. As Mkandawire (1999, p. 133) argues, by offering “little by way of public choices for parties to compete over,” adjustment-era democratization encouraged “precisely those practices it sought to overcome - personalism, factionalism, and clientelism.”

Second, VAT substituted for direct taxation. While VAT reduced volatility (Cagé and Gadenne 2018), it didn’t threaten elite coalition interests, because: farmers paid as consumers, not producers; chiefs collected on transactions, not land; Mouridi’s commercial activities generated VAT, but assets remained untaxed. IFIs’ “modern taxation” framing obscured VAT’s function as alternative to coalition-confronting direct taxation (Riddell, 1992; Cooper, 2002; Boone, 2003; IEO, 2002).

VAT held a further structural appeal that the coalition story alone does not capture. It is the only instrument that reaches the informal economy without requiring the state to register a single income. Informal traders and rural households file no income tax returns, but they bear VAT embedded in fuel, imported goods, cement, and telecoms purchased from the formal sector. This made VAT doubly attractive as it was politically safe with respect to elite coalitions, and administratively feasible given the breadth of informality that direct taxation could not penetrate. Yet as Cagé and Gadenne (2018) show, VAT reaches the informal economy only partially and regressively, which is why the revenue base remained thin and crisis-prone even after its introduction in both countries.

During the SAPs, neither country dismantled coalition veto power, and both relied on indirect taxation. Both returned to fiscal crisis within two decades, indicating that IFI-defined “success” captured short-term stabilization without overcoming developmental hurdles inherited from the colonial era.

The Substitution Pattern in Recent Developments

We have seen that Ghana and Senegal exhibited the same pattern of borrowing substituting for significant revenue reform, despite differences in resource endowments, colonizer, political history, structural adjustment outcomes, and creditor relationships. The constant across both cases is coalition veto power interacting with external financing availability, suggesting these are the significant factors.

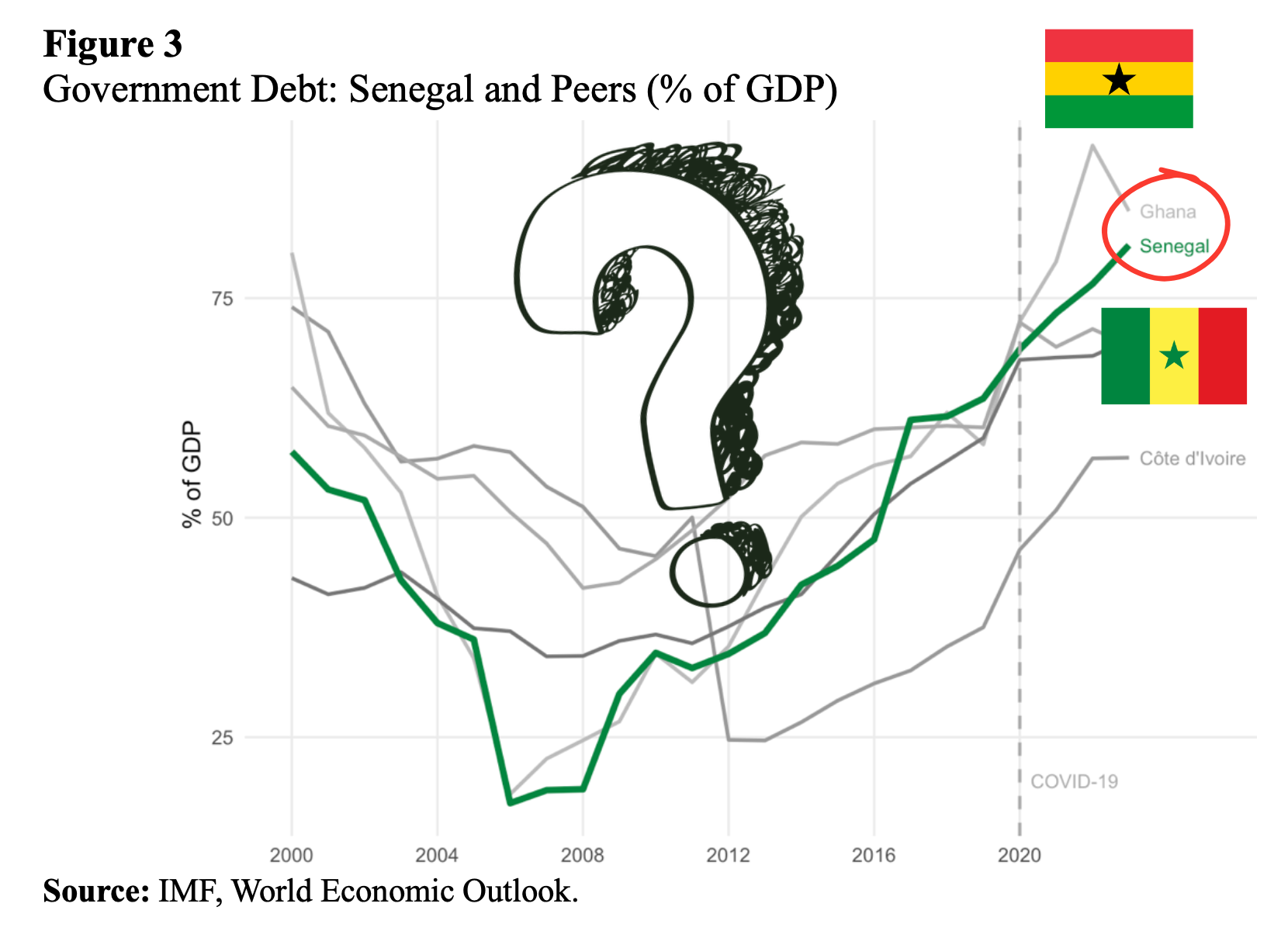

In the period after SAPs, the coalition veto remained paramount. Despite comprehensive HIPC/MDRI debt relief, improved growth conditions, and natural resource discoveries (Ghana’s oil production from 2011) in the 2000s, outcomes reproduced earlier patterns. Ghana’s debt fell to 15 percent of GDP post-MDRI before rising to 50 percent within a decade, while Senegal’s post-HIPC borrowing drove debt ratios upward (IMF 2021, 2022, 2024; Thomas and Giugale2014, pp. 197-198). Rather than financing coalition-breaking reform, fiscal space was again absorbed through renewed borrowing.

This is not a critique of debt relief itself as the HIPC initiative was a necessary intervention that restored breathing room for heavily indebted governments. The point is that fiscal space created by relief was absorbed by the same coalition dynamics that had generated the debt in the first place, because relief addressed the stock of debt without touching the political economy of revenue. HIPC debt relief (2000s) eliminated external debt burden, yet Senegal's “unused HIPC resources” (IMF, 2003) proved insufficient as the government faced political pressure not to confront coalitions.

Ghana consumed its gained fiscal space through grant dependency. Ghana's oil discovery (2011) provided a major revenue windfall - yet direct taxes collapsed to 5-6 percent of GDP as oil substituted for tax reform. Thus, a debt burden and resource scarcity are not persuasive explanations, because in their absence, coalition veto remained the binding constraint on fiscal reform.

A remaining rival explanation would be that perhaps direct taxation stayed low not primarily because of political obstruction, but because the sheer scale of informality made it structurally impossible to tax domestic incomes regardless of political will. It is true that no state can levy income tax on activity it cannot observe, and that both Ghana and Senegal entered independence with economies in which the majority of production and exchange was invisible to the fiscal apparatus. Some portion of the low-direct-tax outcome reflects this capacity floor. Nevertheless the capacity floor explanation cannot account for the trajectory observed. Across the phosphate windfall of the 1970s, the SAP reform windows of the 1980s and 1990s, HIPC debt relief in the 2000s, and Ghana's oil revenues after 2011, neither government invested meaningfully in expanding the administrative reach that would have raised that floor. There was minimal investment in building the registries, formalisation incentives, or taxpayer identification systems that peer countries with comparable informality levels have used to widen their bases. Informality therefore explains the starting point but the coalition veto explains why six decades of fiscal windows left it essentially undisturbed.

So, Has International Borrowing Helped or Hindered Senegal and Ghana in Overcoming Development Hurdles?

Lack of economic development in developing countries has been described as ‘boom–bust’ growth cycles (Jerven, 2011) or as chronic developmental constraint rooted in geography and demography (Bloom, Sachs, Collier, and Udry, 1998). Either of these views is compatible with the argument presented here, because domestic political economy constraints have been found to be the reason for both chronic stagnation and unsustained economic growth following boom cycles.

The sixty-four-year experience of Ghana and Senegal demonstrates that international borrowing substituted for rather than enabled overcoming development hurdles imposed by colonial revenue constraints. Despite comprehensive debt relief, resource windfalls, creditor diversification, and IFI conditionalities explicitly targeting political economic obstacles, neither country achieved fiscal transformation.

Durable domestic coalitions with veto power over direct taxation consistently shaped fiscal outcomes across authoritarian and democratic regimes, favorable and adverse economic conditions, and successive forms of external intervention. This is not a story of uniquely corrupt or incompetent governments. Ghana and Senegal both produced leaders with sound developmental ambitions, from Nkrumah to Rawlings to Senghor. It is a story of structural constraints that made coalition-preserving borrowing the path of least resistance across six decades, regardless of who was in power.

For Senegal, this is a lived reality of today. The 2024-25 audit by the Cour des Comptes, which revealed systematic underreporting of debt averaging 5.6 percentage points of GDP annually under the previous government, is the latest iteration of the same pattern. Borrowed money filled the gap that domestic revenue never closed, and the gap was hidden rather than confronted. The Faye government inherited not just a debt stock but a fiscal state whose administrative reach remains as narrow as it was at independence. The diagnostic exercise in the earlier parts of this series identified electricity as Senegal's binding constraint on private investment and debt as the meta-constraint on the government's ability to fix it. This post suggests the meta-constraint has a political root. This political root is the sixty years of coalition politics that made borrowing repeatedly cheaper than taxing, and each borrowing cycle made the next one more necessary. Breaking that cycle requires not just debt relief or revenue targets. Instead, it requires building the administrative capacity and political coalitions that make direct taxation feasible. That is a harder problem than any SAP conditionality or HIPC framework has so far managed to solve.

Reference List:

Boone, C. (2003). Political topographies of the African state: Territorial authority and institutional choice. Cambridge University Press.

Boone, C. (2012). Territorial politics and the reach of the state: Unevenness by design. Revista de Ciencia Política, 32(3), 623–641.

Bloom, D. E., Sachs, J. D., Collier, P., & Udry, C. (1998). Geography, demography, and economic growth in Africa. Brookings Papers on Economic Activity, 1998(2), 207–240.

Cagé, J., & Gadenne, L. (2018). Tax revenues, development, and the fiscal capacity of states. Journal of Economic Perspectives, 32(4), 1–26.

Cooper, F. (2002). Africa since 1940: The past of the present. Cambridge University Press.

Economist Intelligence Unit. (1965). Quarterly economic review: Annual supplement – Ghana, Nigeria, Sierra Leone, Gambia. Economist Intelligence Unit Ltd.

Economist Intelligence Unit. (1980). Quarterly economic review: Annual supplement – Ghana, Sierra Leone, Gambia, Liberia, . Economist Intelligence Unit Ltd.

Economist Intelligence Unit. (1984). Quarterly economic review of Ghana, Sierra Leone, Gambia, and Liberia (Annual supplement). Economist Intelligence Unit Ltd.

Gardner, L. (2012). Taxing colonial Africa: The political economy of British imperialism. Oxford University Press.

International Monetary Fund. (1995). Ghana – Background information on output and investment performance (IMF Staff Country Report No. 95/78). International Monetary Fund.

International Monetary Fund. (2003). Senegal: 2002 Article IV consultation and requests for a three-year arrangement under the Poverty Reduction and Growth Facility and for additional

interim assistance under the Enhanced Initiative for Heavily Indebted Poor Countries – Staff report (IMF Country Report No. 03/167). International Monetary Fund.

International Monetary Fund. (2021). Ghana: 2021 Article IV consultation—Staff report (IMF Country Report No. 21/165). International Monetary Fund.

International Monetary Fund. (2022). Senegal: 2021 Article IV consultation, fourth review under the Policy Coordination Instrument (IMF Country Report No. 22/8). International Monetary Fund.

International Monetary Fund. (2024). Ghana: 2024 Article IV consultation – Staff report (IMF Country Report No. 24/334). International Monetary Fund.

Independent Evaluation Office of the IMF. (2002). Evaluation of prolonged use of IMF resources. International Monetary Fund.

Jerven, M. (2010). African growth recurring: An economic history perspective on African growth episodes. Economic History of Developing Regions, 25(2), 127–154.

Koddenbrock, K. (2024). Earnest struggles: Structural transformation, government finance, and the recurrence of debt crisis in Senegal. Review of International Political Economy, 31(5), 1795– 1821.

Mamdani, M. (1996). Citizen and subject: Contemporary Africa and the legacy of late colonialism. Princeton University Press.

Mkandawire, T. (1999). Crisis management and the making of “choiceless democracies.” In R.

Joseph (Ed.), State, conflict, and democracy in Africa (pp. 119–136). Lynne Rienner.

Mkandawire, T. (2001). Thinking about developmental states in Africa. Cambridge Journal of Economics, 25(3), 289–313.

Riddell, J. B. (1992). Things fall apart again: Structural adjustment programmes in sub-Saharan Africa. Journal of Modern African Studies, 30(1), 53–68.

Thomas, A., & Giugale, M. (2014). Achieving debt sustainability in emerging markets. World Bank.

World Bank. (1989). The World Bank and Senegal, 1960–87 (Report No. 8041). Operations

Evaluation Department. 12